The Ultimate Guide to SIP Investment in India: Everything You Need to Know (2026)

Highlights

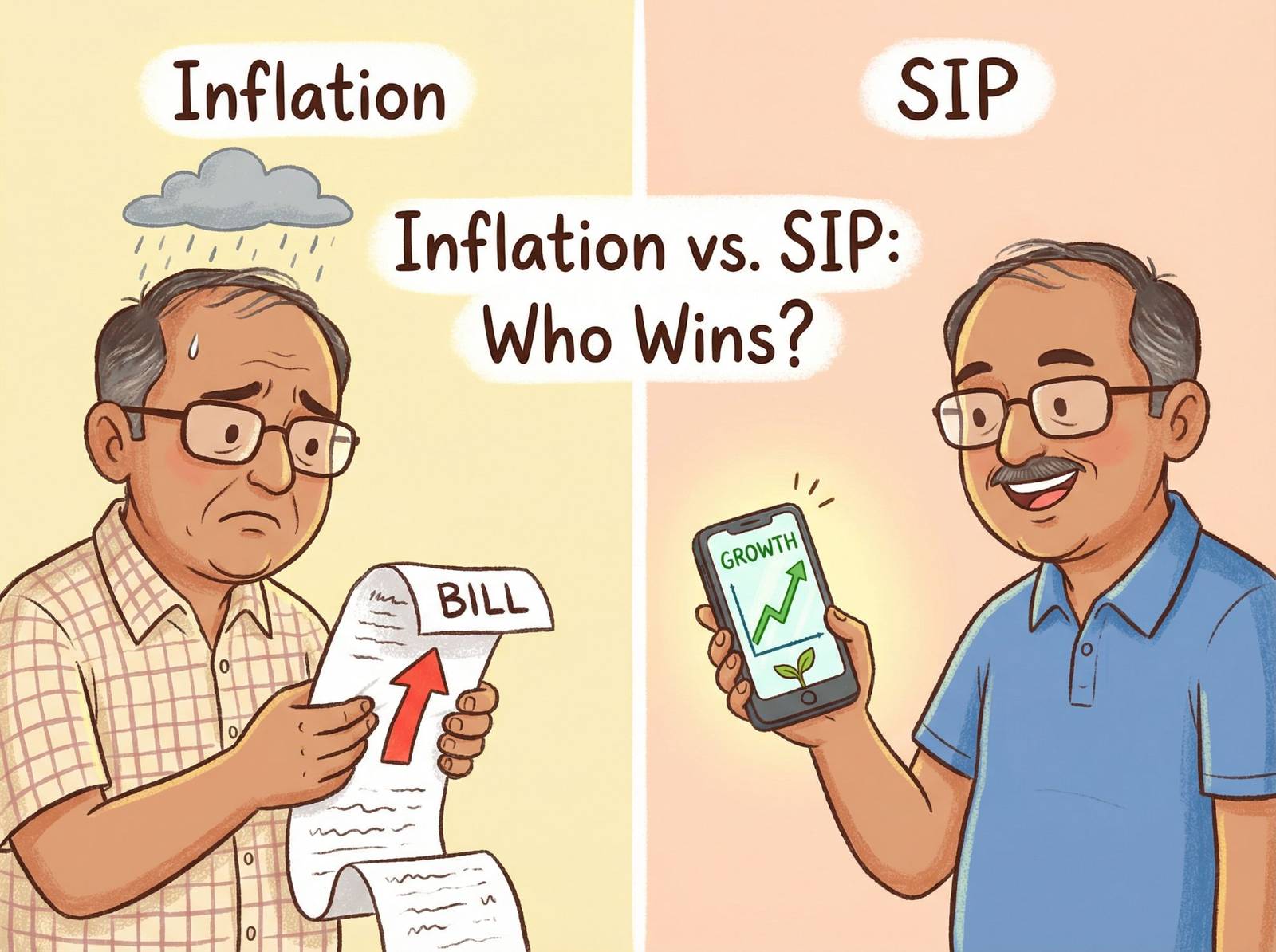

Meet Shankaran Pillai.

Shankaran lives in Kallakurichi. He is a careful man. He wears a helmet even when walking to the corner shop. For 20 years, he has put every spare Rupee into a Bank Fixed Deposit (FD) or a Post Office Recurring Deposit (RD).

But lately, Shankaran is worried. The price of milk has gone up. Petrol is expensive. His FD interest rate is barely covering inflation. He keeps hearing his nephew talk about “SIP” and “Market Returns,” but Shankaran is scared. He thinks the stock market is a gambling den.

If you are like Shankaran—hardworking, cautious, but worried your savings aren’t growing fast enough—this guide is for you.

We are going to break down Systematic Investment Plans (SIP) in simple Indian English. No jargon. No confusion.

What is a SIP? (The Simple Definition)

Is SIP a product? No. SIP is a method of investing money.

Think of it like this:

- Mutual Fund: This is the vehicle (like a bus) that takes your money to the stock market.

- SIP (Systematic Investment Plan): This is the ticket buying process. You buy a ticket every month automatically.

In technical terms, a SIP allows you to invest a fixed amount (e.g., ₹2,000) at regular intervals (usually monthly) into a Mutual Fund scheme. It is exactly like a bank Recurring Deposit (RD), but the money goes into the market instead of a bank vault.

Key Features of SIP:

- Flexibility: Start with as little as ₹500.

- Automation: Money is deducted from your bank automatically (Auto-debit).

- Discipline: You invest regardless of whether the market is up or down.

SIP vs. Mutual Fund: Are They the Same? Simple Explanation

Why Choose SIP Over FD or RD?

Shankaran loves his FD because it feels safe. But is it financially safe?

Here is the math. If inflation in India is 6% and your FD gives you 7%, after paying tax, you are actually losing purchasing power. SIPs in Equity Mutual Funds are designed to beat inflation over the long term (5+ years).

Comparison: SIP vs. Traditional Savings

| Feature | Bank RD / FD | Equity SIP |

| Average Returns | 6.5% – 7.5% | 12% – 15% (Long Term) |

| Risk | Low | Moderate to High |

| Liquidity | Penalty on premature withdrawal | High (Exit load may apply < 1 year) |

| Taxation | Taxed as per income slab | 12.5% LTCG (Above ₹1.25 Lakh profit) |

| Inflation Beating? | No (Barely matches it) | Yes (Builds wealth) |

Data Source: Historical market performance of Nifty 50 vs. SBI FD Rates (2014-2024).

5 Reasons Why SIP is Better Than Recurring Deposit (RD)

How SIP Works: The Magic of “Rupee Cost Averaging”

This is a fancy term for a simple concept. Let’s explain it the way Shankaran buys onions.

When onion prices are high (₹80/kg), Shankaran buys only half a kg. When prices drop (₹20/kg), he buys 2 kgs.

SIP does the exact same thing for you automatically:

- Market Crash: Net Asset Value (NAV) is low ➝ Your ₹5,000 buys More Units.

- Market Peak: NAV is high ➝ Your ₹5,000 buys Fewer Units.

Over time, your average cost of buying remains low. You don’t need to time the market. You don’t need to watch the news. You just need to keep investing.

The Power of Compounding: How to Make ₹1 Crore

Albert Einstein called compounding the “Eighth Wonder of the World.” In India, we call it the “Money Making Money” scheme.

If Shankaran starts investing ₹10,000/month at age 30, assuming a 12% return, look at what happens by age 50:

- Total Money Invested: ₹24 Lakhs

- Interest Earned: ₹75.9 Lakhs

- Total Value: ₹99.9 Lakhs (~1 Crore)

If he waits just 5 years to start (starts at age 35), he would need to invest nearly ₹18,000/month to reach the same goal. The cost of delay is massive.

How to Use a SIP Calculator to Plan Your ₹1 Crore Goal

Types of SIPs Available in India

Not all SIPs are the same. Choose the one that fits your salary structure.

1. Regular SIP

The classic. You invest a fixed amount (e.g., ₹5,000) on a fixed date (e.g., 5th of every month).

2. Step-Up (Top-Up) SIP (Highly Recommended)

You increase your SIP amount automatically every year.

- Example: Start with ₹5,000. Increase by 10% next year (₹5,500).

- Why: As your salary grows, your investments should grow too. This accelerates your journey to ₹1 Crore by years.

3. Perpetual SIP

No end date is selected. The SIP continues until you send a request to stop it. This is best for long-term retirement goals.

Is SIP Safe? (Risk vs. Reward)

Is your money guaranteed? No.

Unlike an FD, SIP returns fluctuate daily.

Is it safe? Yes, if you follow the rules.

Mutual Funds are strictly regulated by SEBI (Securities and Exchange Board of India). The fund house cannot run away with your money.

However, the market will go up and down.

- Shankaran’s Fear: “What if the market crashes tomorrow?”

- The Reality: If the market crashes, your SIP buys more units at a “discount.” When the market recovers (which it historically always does in India), those cheap units explode in value.

Top 7 Mistakes to Avoid When Starting Your First SIP

Taxation on SIPs (Updated for 2026)

The government wants a share of your profit. Here is the tax structure for Equity Mutual Funds (where >65% is invested in stocks), based on recent budget updates:

- STCG (Short Term Capital Gains):

- If you sell before 1 year.

- Tax: 20% on profits.

- LTCG (Long Term Capital Gains):

- If you sell after 1 year.

- Tax: 12.5% on profits exceeding ₹1.25 Lakhs in a financial year.

- Note: Profits up to ₹1.25 Lakhs per year are tax-free.

Tip: Don’t withdraw money frequently. Let it grow for 5+ years to minimize tax impact.

How to Start a SIP Online: A 3-Step Guide

You do not need to visit a bank branch or sign physical papers anymore.

Step 1: Get KYC Compliant

You need your PAN Card and Aadhaar linked to your mobile number. You can do “e-KYC” on any major investment platform (Zerodha, Groww, Coin, or directly via AMC websites).

Step 2: Choose the Right Fund

For beginners like Shankaran, an Index Fund (Nifty 50) or a Flexi-Cap Fund is usually the safest starting point. These funds invest in India’s top companies.

Step 3: Set Up Auto-Pay

Link your bank account. Set the deduction date for the day after your salary usually hits (e.g., the 7th of the month).

How to Start SIP Online in India: Step-by-Step Process (2026)

Conclusion: Don’t Be a “Waiter”

Shankaran Pillai spent 5 years “thinking about it.” In those 5 years, the Sensex moved from 40,000 to over 80,000. He missed the rally.

Investing is not about timing; it is about time in the market.

- Start small (₹500).

- Start now.

- Ignore the noise.

Ready to see how much wealth you can build?